Overlooked Sector Faces New Tax Gauntlet as Compliance Crackdown Overshadows Reliefs

A Sector Overlooked Faces a New Regulatory Gauntlet

For the UK’s charity sector, Chancellor Rachel Reeves’ November 2025 budget offered “little to celebrate,” deepening a widespread feeling of being “overlooked and underrecognised” by the government. While sector bodies expressed disappointment at the lack of significant financial support during an intensely challenging period, the budget’s pages concealed a more profound story. Beyond the headlines, the government finalised a complex package of new tax compliance and accounting rules set to take effect in 2026. This matters profoundly. While direct fiscal support was absent, these technical changes will fundamentally reshape the regulatory landscape for charities. At a time of mounting economic pressure, the new rules will demand greater diligence and more rigorous record-keeping in financial management, investment strategy, and donor relations, presenting a new gauntlet for organisations to navigate.

A Mixed Bag of Reforms: New Reliefs Tempered by Tougher Compliance

The government’s recent announcements represent a dual-edged sword for the third sector. While one long-lobbied-for tax relief has been confirmed, it arrives alongside a suite of anti-avoidance measures designed to strengthen compliance and “close the tax gap.” This creates a landscape of both opportunity and increased scrutiny.

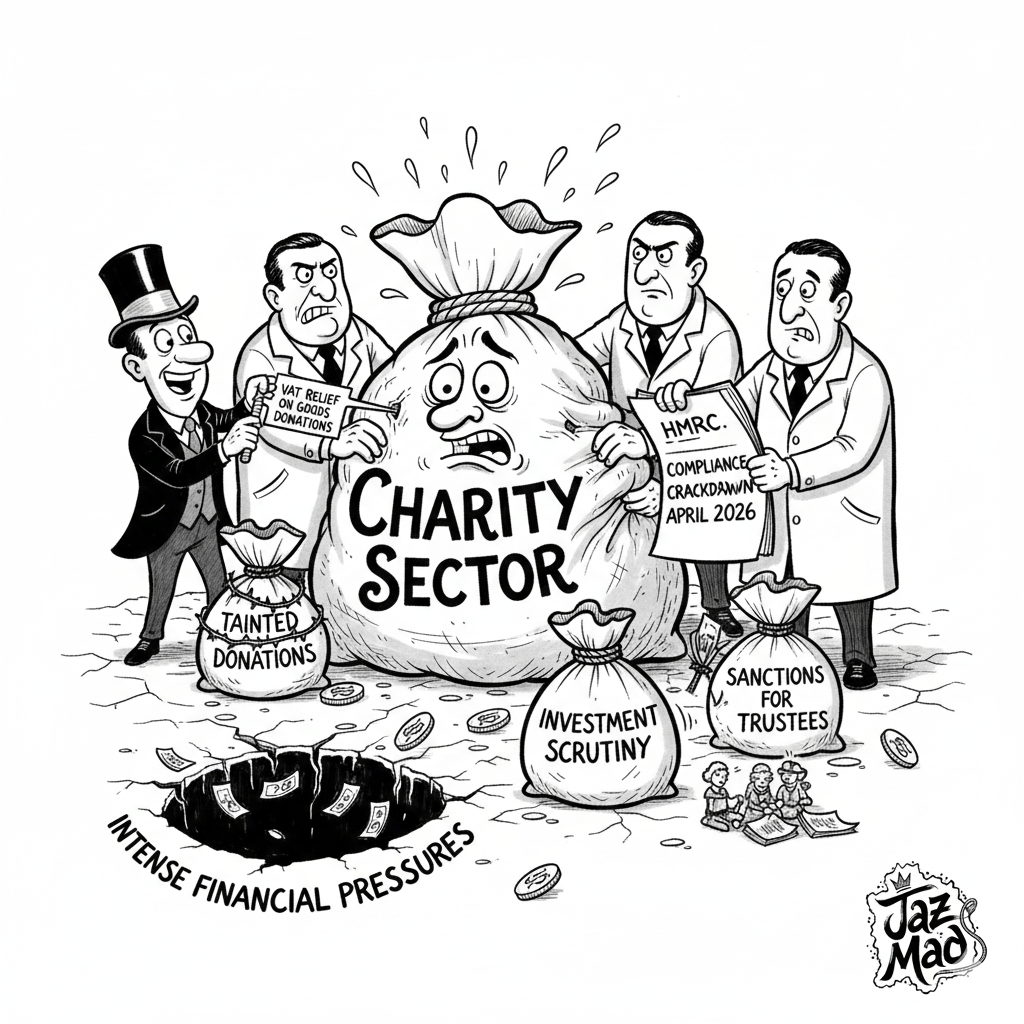

On the positive side, the budget confirmed the introduction of VAT relief on business donations of goods, a move broadly welcomed by the sector. Richard Bray, Chair of the Charity Tax Group (CTG), celebrated the confirmation, hoping it would “bring benefits to those in most need of help.” Similarly, Clare Mills, co-CEO of the Charity Finance Group (CFG), welcomed the policy, particularly the government’s decision to set a higher value limit of £200—up from a proposed £100—for certain high-value donated items such as technology, furniture, and household appliances.

However, this relief is tempered by the government’s primary focus: a significant crackdown on tax avoidance. A package of four key changes, scheduled to take effect in April 2026, will tighten the rules considerably:

- Tainted Donations: The rules for identifying improper donations are being fundamentally altered. The current test, which relies on the donor’s subjective ‘motivation,’ will be expanded into a more robust, two-part test that also considers the transaction’s objective ‘outcome’. Critically, the threshold is being lowered from a donor receiving a “financial advantage” to the much broader “financial assistance,” a term that can include loans or investments, even if made on arm’s-length terms.

- Approved Investments: Previously, only one of the twelve approved categories of charitable investment was subject to a strict requirement that it be made for the “sole purpose of benefitting the charity” and not for tax avoidance. This rule is now being extended to all twelve categories, creating a uniform standard but also subjecting a wider range of investment decisions to potential HMRC scrutiny.

- Attributable Income: The definition of “attributable income,” which is used to calculate a charity’s tax relief, will be expanded to include legacies. This means that funds received from bequests must be spent on the charity’s core purpose; otherwise, they could be subject to a tax charge.

- New Sanctions: HMRC is developing new powers to sanction non-compliant trustees and managers. These will be implemented through changes to the guidance for the “fit and proper persons” test, a move described as a potential “very big stick” to compel compliance with tax obligations, such as timely filings.

Taken together, these four changes represent a significant tightening of the regulatory screws, shifting the burden of proof onto charities and demanding a new level of diligence in their day-to-day financial governance. This underscores the need for sector leaders to feel empowered and prepared for upcoming compliance challenges.

Sector Impact: A Rising Tide of Administrative Scrutiny

While HMRC states these compliance measures target a ‘minority,’ their practical effect will be to raise the standards for financial governance and record-keeping across the entire sector. Trustees and finance managers must respond proactively to these changes to avoid falling foul of the stricter regime, making awareness and preparation essential.

Analysis from legal experts at Macfarlanes suggests that charities must now ensure meticulous record-keeping, particularly regarding the rationale for investment decisions, which should be carefully documented in trustee meeting minutes. The changes to inheritance tax rules have also been met with caution. While welcoming the policy’s intent, the CTG’s Richard Bray noted the need to “ensure that there are no unintended consequences” for legacy income, which remains a vital funding source for many organisations.

This tightening of compliance is not happening in a vacuum. It sits alongside a seemingly contradictory move to reduce the administrative load for smaller charities. These are not paradoxical, but rather represent a deliberate, dual-track government strategy. The deregulation, which will raise the income threshold for a full audit to £1,500,000 from September 2026, is targeted at reducing the day-to-day burden on smaller charities and making their operations more proportionate. In contrast, the compliance crackdown is a sector-wide, anti-abuse measure aimed at financial integrity. The government is simultaneously easing administrative requirements for the smallest players while raising the bar on tax compliance for everyone.

Adding to this complex picture is the introduction of the new Charities SORP (Statement of Recommended Practice) 2026. The updated SORP will bring detailed guidance on reporting financial reserves and ESG issues, requiring charities to stay informed and adapt their reporting practices. Navigating these reforms alongside increased scrutiny underscores the importance of sector awareness and proactive planning.

The Bigger Picture: A Call for Recognition in Challenging Times

The technical nature of these tax changes belies a deeper frustration within the sector. In the words of Leigh Brimicombe, an executive at NCVO, charities remain “overlooked and underrecognised” despite adding billions to the economy and being “essential to local growth, neighbourhood health and community connection.” This lack of acknowledgement in the budget comes at a particularly “challenging time.”

Organisations are grappling with the impact of rising minimum wage rates on their payrolls, a cost not matched by any new government funding. Furthermore, as Sarah Lomax, co-chief executive of CFG, pointed out, the government’s decision to freeze the income tax threshold could increase demand for charity services as household budgets are squeezed. Lomax aptly described the budget as a “mixed bag” that contained “little to ease the concerns around the financial sustainability of the sector.” Her assessment captures the prevailing mood: any positive developments are overshadowed by the immense operational and financial pressures charities currently face. The sector’s focus must now shift from reacting to the budget to preparing for the significant regulatory changes ahead.

Preparing for 2026 and Beyond

Ultimately, the UK charity sector is entering a new era defined not by new funding but by new rules. The November 2025 budget has set the stage for a period of significant regulatory adjustment, where welcome reliefs and administrative simplifications for smaller organisations are overshadowed by a substantial tightening of tax compliance that will affect all. This central tension will require careful navigation and robust preparation. For charity leaders, trustees, and finance teams, the immediate task is to fully understand the implications of these changes and implement the necessary internal processes to ensure compliance by the April 2026 deadline. As the NCVO has made clear, the longer-term goal remains to “work with Treasury to ensure future budgets reflect the value charities bring.” For now, however, the sector’s energy must be directed inward, preparing for a more demanding and scrutinised future.