New Charity Accounting Rules on Impact Reporting Draw Criticism

The Coming Shift in Charity Accountability

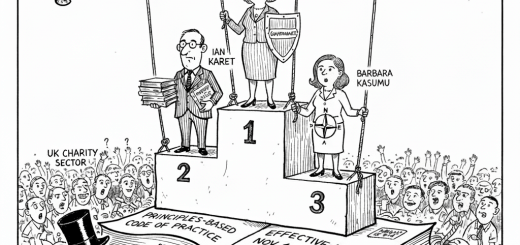

A profound shift in accountability is on the horizon for the UK charity sector. A new mandatory impact reporting rule, part of the forthcoming Charities Statement of Recommended Practice (SORP), will become a requirement for all charities for accounting periods beginning after 1 January 2026. While regulators envision this as a pivotal opportunity for more meaningful communication, sector leaders are raising urgent concerns that it could become yet another administrative burden. David Holdsworth of the Charity Commission sees a chance for organisations to tell their story, but Debra Allcock Tyler from the Directory of Social Change warns of the practical difficulties many charities will face. This is more than just an accounting adjustment; it represents a fundamental change in how charities will be required to define, measure, and justify their value to trustees, funders, and the public they serve.

The Heart of the Matter: A Mandate for Impact

For charity leaders, understanding the specifics of this new mandate and the key voices shaping the debate is crucial for navigating the upcoming changes strategically. The new Charities SORP will make impact reporting a mandatory requirement, shifting it from a best-practice recommendation to a core compliance element for all charities starting after 1 January 2026, highlighting its significance for strategic planning.

The regulator’s perspective, articulated by Charity Commission CEO David Holdsworth, is one of ambitious reform. He has emphatically warned that the new rule “can’t just be an annual tick-box.” Drawing a parallel to existing public benefit statements, he criticised the current state of reporting, lamenting what he called an:

“awful paragraph that I see cut and pasted across tens of thousands of charity annual returns, which says: ‘We the trustees confirm we comply with the public benefit.’”

In Holdsworth’s view, such boilerplate language causes charities to immediately lose their audience and fail to convey their true value. His vision is for organisations to become “deliberate” about their reporting, using it as a powerful opportunity to explain the “fantastic work you are doing, the impact you are having”. This perspective aims to inspire charity leaders and trustees to see impact reporting as a meaningful way to showcase their mission and motivate continued effort.

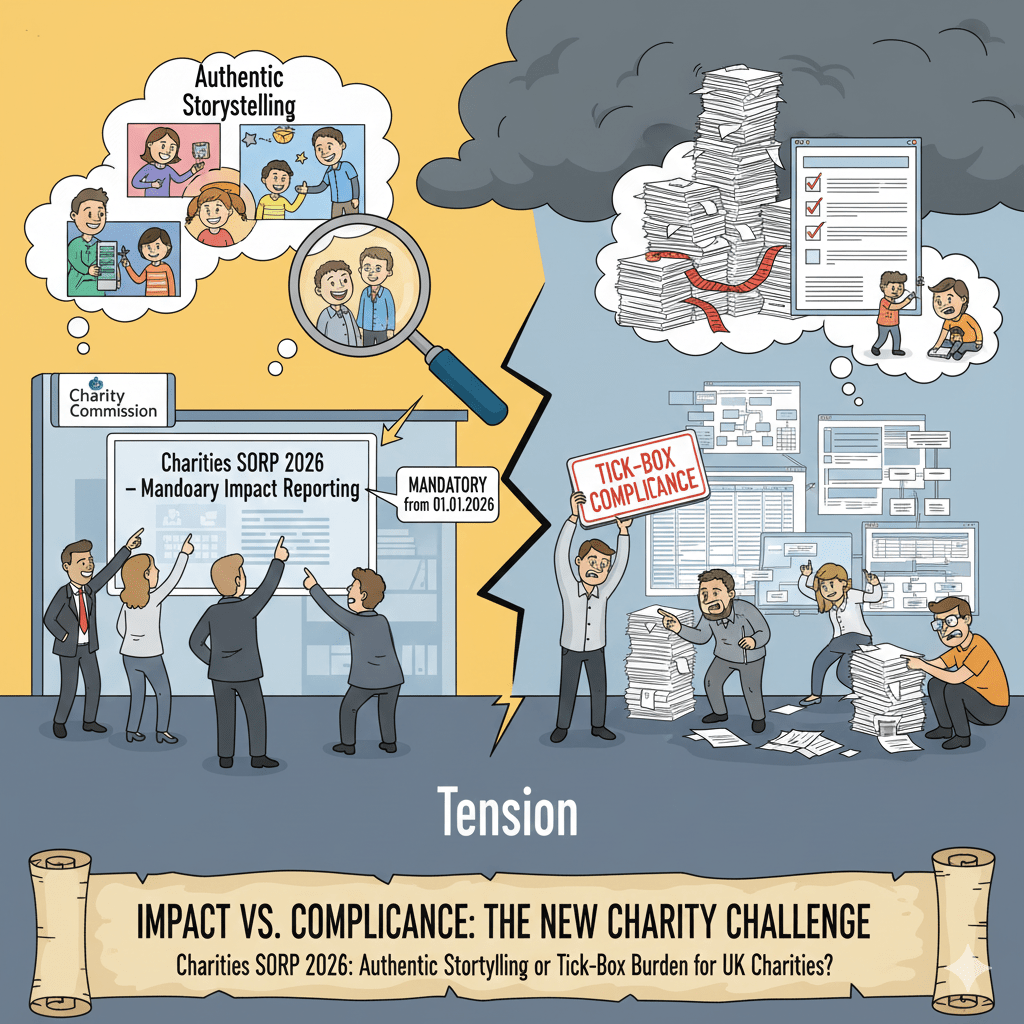

A Contentious Requirement: Fears of a Tick-Box Exercise

Understanding the practical criticisms of the new requirement is strategically vital, as they highlight the real-world challenges that could undermine its very purpose. For example, many charities lack the tools or data collection systems needed to measure impact effectively, which deepens concerns that the mandate could lead to superficial or boilerplate statements, as voiced by Debra Allcock Tyler.

This criticism directly challenges the regulator’s vision. It suggests that, far from inspiring authentic narratives, the mandate could inadvertently create the very “tick-box” exercise that David Holdsworth is trying to eliminate. The core of the debate is a clash between the ideal of genuine impact storytelling and the fear of a compliance-driven, boilerplate response. For many organisations, especially smaller charities with limited resources for dedicated impact measurement, the pressure to comply may overshadow the opportunity to communicate, potentially leading to generic statements that satisfy the rule but fail to capture the unique value of their work, a tension that is not unique to the UK but reflects a wider, global conversation about non-profit accountability.

A Global Trend: The Push for Greater Transparency

The UK’s new SORP rule is not an isolated development. It reflects a much larger international movement to standardise how non-profit organisations (NPOs) report their financial and non-financial performance. The global context for this shift is the International Financial Reporting for Non-Profit Organisations (IFR4NPO) project, a major initiative aimed at the development of internationally applicable financial reporting Guidance for non-profit organisations. This global trend can instil confidence in sector leaders that they are part of a broader, positive movement towards transparency and accountability.

The core problem IFR4NPO seeks to solve is the current lack of common international accounting standards for NPOs. This absence has forced donors to create their own varied financial reporting requirements, creating a “heavy burden” for charities that must navigate different rules for different funders and jurisdictions. The project’s key objectives are to strengthen governance and build trust by improving the quality, transparency, credibility, and comparability of NPO financial reports.

Crucially, the IFR4NPO project emphasises that robust accountability requires more than just numbers. It explicitly states that financial reports must be combined with “narrative, non-financial information” that provides an understanding of an entity’s objectives, strategy, risks, and performance. This ‘narrative reporting’ is designed to complement financial data, providing crucial context that allows stakeholders to assess not only financial health but also whether an NPO is achieving its objectives efficiently and effectively. This mirrors the UK’s push for mandatory impact reporting, confirming that the change is part of a coherent global trend. With the IFR4NPO’s final guidance anticipated in mid-2025—just ahead of the UK’s 2026 implementation date—the direction of travel is clear.

A Challenge and an Opportunity

The introduction of mandatory impact reporting presents the charity sector with a classic dilemma: the tension between an ambitious goal and the significant practical challenges of implementation. This change is far more than a new line item in an annual report; it is a strategic imperative for every charity to get better at defining, measuring, and communicating its unique value. The risk of this becoming a hollow compliance exercise is real, but so is the opportunity for deeper engagement and stronger storytelling. As David Holdsworth notes, conversations about credible impact “should already be happening within trustee boards anyway.” This serves as a powerful call to action. To avoid the pitfalls, the sector must be proactive. By becoming “deliberate” in their approach now, charities can take ownership of their impact narrative and transform a potential compliance headache into a strategic advantage.